One of my clients recently asked me if he should make monthly prepayments on a mortgage for an apartment building he owns. He bought this property a few years ago and has worked hard to turn it into a profitable investment. As it looks right now, he estimates he’ll have monthly positive cashflow of $2,850.

He was considering his options for this monthly cashflow and wanted to know my thoughts on mortgage prepayment. He shared that his interest rate was 5.375% and sent me his loan amortization schedule. At first, I told him he could probably get a better return on investment investing the cashflow into other assets. If he got a return on this monthly cashflow above 5.375%, he would be better off. (This isn’t factoring in the tax savings on the mortgage interest. I do realize his actual out of pocket cost for the mortgage interest is less than 5.375% because of the tax deduction.)

For some reason, I spent some time studying this amortization schedule and have come to a different conclusion. It’s crazy, but I’ve owned real estate for many years as an investor and have never really studied an amortization schedule. I was also a CPA for many years before I got into real estate and still never really examined amortization schedules. I always focused on the mortgage interest rate and made all decisions around this one figure. If the mortgage interest rate was higher, it was a good idea to make prepayments. If the mortgage rate was lower, it was better to make the minimum payment and use the funds in other investment opportunities.

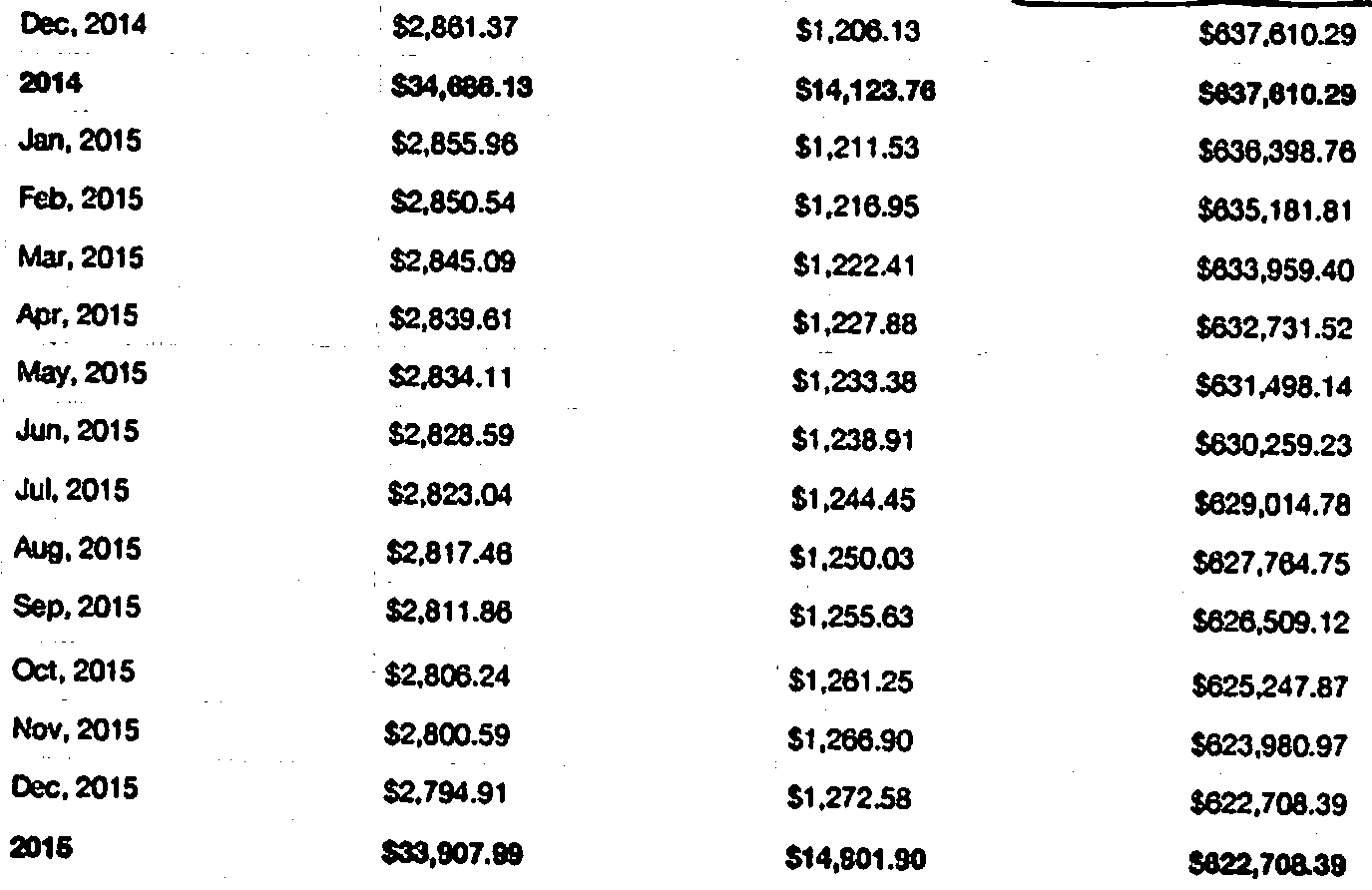

Well, I’m starting to rethink this after looking at this amortization schedule. Here’s an ugly screenshot from this amortization schedule:

The total monthly mortgage payment is $4,067, which includes principal and interest. The left column shows the portion of the payment allocated to interest each month. The next column shows the portion of the payment allocated to the principal each month. The column on the far right shows the outstanding principal balance after each monthly payment is applied. You can see the annual totals for each column in bold for 2015 in the bottom row.

In the book “Wealth Without Risk” by the late Charles Givens, he recommended the following:

“On the first of the month when you write your regular mortgage check, include an additional payment equal to the principal portion of the next month’s payment.”

This recommendation would allow anyone to pay off their mortgage payment in half the time. In the amortization schedule above, this investor would make their regular December 2014 mortgage payment of $4,067 plus the principal portion of the payment for January 2015 of $1,211.53.

This loan has 272 remaining payments (22.6 years) according to his amortization schedule. By following this prepayment plan, the investor will shave 136 monthly payments off of the mortgage and will have this apartment complex paid off in full in 11.3 years. At this point, he’ll add $4,067 to his monthly cashflow.

Not too bad, if you ask me.

Here’s what caught my attention about the amortization schedule. If this investor did make the extra principal payment for January 2015 of $1,211.53, he would eliminate this payment from the amortization schedule as the outstanding principal balance would drop down to the outstanding balance after the January 2015 is applied of $636,398.76.

If we look at this month of January 2015, we’ll see that his additional prepayment in December 2014 actually removes the interest portion of the January 2015 payment. This means his $1,211.53 additional principal prepayment in December saves him $2,855.96 of interest in January.

Is this correct?

If so, I’ve been missing out on an amazing investment opportunity. Maybe you have too?

Who wouldn’t want to invest $1,211.53 one month for a guaranteed $2,855.96 in the very next month? This is a guaranteed 135.7% return on the investment.

In fact, if this investor were to make one lump sum principal prepayment of $14,801.90, which represents the total principal to be paid down in 2015, he would save $33,907.99 in interest. (Refer to the bold totals for 2015.) This lump sum prepayment would move him down to January 2016 outstanding principal balance in the amortization schedule.

This would be a 129% annual return on his investment calculated as follows:

Total interest saved $33,907.99

Less principal prepayment of ($14,801.90)

Gain on investment (actual interest saved) $19,106.09

ROI (Divide the Gain by Amount Invested) 129% ($19,106.09 divided by $14,801.90)

I’m writing this at 5:45 am and have been up working for awhile. I might be delusional. 🙂

Is it possible to make 129% guaranteed prepaying a mortgage with a 5.375% rate?

What do you think? Is this thinking correct, or am I missing something?

13 replies to "Prepay Your Mortgage? Could this be the best guaranteed investment we can make?"

We did just that and paid a 5% interest 24 remaining year amortized mortgage of $101,500 off in a little over 3 years. Saved $65,277.34 in interest. I am in commission sales, and every dollar I could spare went straight onto the principal of the mortgage. Full principal and interest payment check on the first of the month, plus principal amounts for the next few months added together to total whatever I could spare, but never less than 2 extra months principal payment in a separate check market principal payment only. We just zoomed to the bottom line.

would have never saved that much in such a short time or since. It just got addictive to see the balance get smaller and smaller.

Rita

[…] This is a long post, but if you’re serious about saving money over the long term, I think you’ll find this to be a good read. […]

Since yesterday morning, I’ve gotten many comments here on the blog and more emails about prepaying a mortgage. I’ve thought this investment opportunity more after reading each email and every comment.

Here’s the conclusion I’ve come to…

Prepaying a mortgage is one of the best guaranteed investments anyone can make IF they are investing for the long-term and they have other investments or savings set aside for their retirement.

The reason why prepaying a mortgage is the best guaranteed investment is because you do save a significant amount of money. The outstanding principal balance on the amortization schedule is the golden number. By prepaying one month of principal in advance, you move the outstanding principal balance down an entire month saving an entire month’s worth of interest. If this client followed this approach, his monthly investment to prepay this mortgage would guarantee him $551,485 in 11 years.

He wouldn’t have to worry about the stock market crashing, real estate values plummeting, or bonds falling when interest rates rise. This return is guaranteed. There is a great deal of “peace” in this guaranteed return considering what we’ve been through over the last 10 years.

The challenge is that the prepayments are not liquid as many of you have suggested. If he wants, or needs, these prepayment funds at any point, he can’t access them. The funds are locked up in the property. He’ll have to wait 11.3 years to feel the benefit of this monthly investment. He is in his mid 40s and likes the idea of having this property paid off in full before he turns 60.

In addition, he also loses any potential gain from investing into other assets like an index fund. He could simply invest his monthly cashflow in a low cost index fund mirroring the market and let it compound for 11 years. If he invested his monthly cashflow of $2,850 into a fund averaging 8% over the 11 years, his investment would grow to $593,654, which is slightly higher.

The problem is there is no guarantee on this investment. He could lose money if the market crashes (which it certainly will) at some point in the next 11 years. He has to average 8% a year in order to achieve this result.

Maybe the best strategy is to split the positive cashflow 50/50 and use one half to make monthly prepayments and the other half as a savings reserve, or index fund investment. His monthly cashflow is $2,850 and he could prepay $1,425 each month and save/invest $1,425 each month.

He would benefit greatly from both approaches. He would have a guaranteed return on 50% used for mortgage prepayment plus the possibility of higher returns and liquidity with the other 50%.

Prepaying a mortgage is a much better investment opportunity than most people realize. It really is. About half of the comments and emails I received seemed to downplay the idea. I think this is a knee jerk reaction. You really have to analyze the amortization schedule and think accurately.

It all boils down to each person’s situation. Does he have other reserves to handle repairs? Does he have other savings outside of this apartment complex? Is he willing to invest for 11 years without a penny coming back to him? If so, prepaying a mortgage is an incredible investment opportunity.

Rob, I tell my buyers how to pay off a 30 Yr. mortgage in 15 years without being obligated to do it as with a 15 Yr. mortgage. One day I was just finished with a closing and we had the lenders’ amortization schedule and I demonstrated exactly what you described but the loan officer was there and he said NOOooo! So, my brother in law is a MENSA member, an engineer and a computer guy in the aeronautical business working on computers and the predecessor to the Internet that Al Gone created, and so I gave him an example of a 30 yr. loan at a couple hundred thousand at some normal rate on the loan and asked him to do this problem and pay the next principle amount and pay it on the 1st of each month and see when the principal balance was paid off. When he gave me the printout results a few days later it was paid off in 180 months except for less than $1.00 in change to be paid. The key is to pay exactly on the 1st and to write a separate check and a note to please pay down my principle balance and then hover over the bank and prove every time that they did not credit your principle as requested and confront them in a timely manner. Of course the loan must not have any restriction on pre-payment. I don’t know if any of my buyers have followed this plan but most of them say they want to prepay some amount, maybe $!00. or so. It’s important to know also tha any pre- payment wil yield more equity. when you sell, even if you don’t finish the schedule. FUN Dave Jones

My husband taught this to me 29 years ago! By taking your monthly P & I and adding any amount designated as “principal” you now have reduced your interest significantly. Using your example of Dec. pymnt. + principal of next month’s pymnt. you have just eliminated that whole months interest and the interest is now calculated on the new principal balance. I have shown this to several who really don’t believe it, but work it out with a calculator with different amounts and it comes out right every time. The key is to designate the extra $ amount as “principal” when paying your monthly payment. And remember you still have to pay every month. “Prepaying” this way does not prevent you from acruing penalties & additional interest if you skip payments. You must still make monthly payments. The beauty of it is that you are saving tons in interest.

Hey Rob,

Great advise and we do this but you can’t get away from that interest payment although you

can certainly lower it a little by paying the principle early and paying the loan off early. You made me do some math!

Marianne

Run an amortization chart on the new payment schedule and you can see the actual results. Either way lump sum or additional monthly payments.

All mortages will have the wording something like “payment will be applied FRIST to interest on the outstanding balance and then applied to the principle reduction.”

These strategies work! I have a financial services company and I’ve been in the real estate industry for over 23 years and have advised many clients on this very strategy. Of course it should be calculated for each individual client based on their goals. It can also work much faster if you pay more of a principle payment for reduction. It can drastically reduce the amount of interest you pay and the years you pay on your loan.

Rob your results of 129% should be accurate. Think of it this way, someone paying on a mortgage amortized over 30 years at 6% ends up paying approximately 116% total interest on the money borrowed when all is said and done! Amortized interest is front end loaded-compounding interest.

To learn how to earn compounded interest instead of paying it please visit my web site at; http://www.InfiniteWealthInc.com, my book also explains compounded interest and more investment strategies at; http://www.KnowYourFinancialFreedom.com

Joe Militello

Author

Wealth Strategist

Hi Rob,

All of your numbers appear to be correct. However, we need to be careful as to what meaning we assign to the calculations and the numbers we are looking at. Here’s what I mean…

It’s simplest to islolate a single prepayment and examine what’s going on — let’s use the Jan 2015 payment. It’s true, make an extra $1211 payment in December 2014 and you save the $2855 scheduled interest in January. But, you don’t realize that savings right away. You save that money on the back end of the transaction, years down the road. Now, the February 2015 payment essentially becomes the January 2015 payment and you owe $2850 — a savings of $5.

Now don’t despair, it sounds bad but it really isn’t. That $5 savings will roll through the rest of the amortization schedule, keeping your principal reduced by $1211 + the compounded benefit of the acceleration. If we ran the numbers, it would work out to an annualized return of 5.375% or so (not taking into consideration any tax benefit of the interest).

So, you were correct in your original assumption that prepaying a 5% mortgage gives a return of 5% — in the form of interest savings, and less if we consider tax benefits.

But, this is only half the story. Something else to consider is the fact that equity in the property has no rate of return. So, we would be “investing” money to wipeout future interest with no corresponding current return or cashflow benefit (pre-paying the mortgage won’t reduce the monthly payment, just shorten the amortization schedule)– and actually it’s negative cashflow event because the prepayment funds had to come from somewhere.

Assuming you could earn more than the cost of the 5.375% mortgage (again, not considering tax benefit), you’d be better off “storing” the money there (call it a side-fund), than storing it in the property in the form of equity. Presumably, you’d put it somewhere it could earn a return to offset/cancel the interest paid on the mortgage, and allow the money to compound so over time it would grow and turn into increased cashflow.

Then, at some future point, if you wanted to or needed to, you could use the side-fund to payoff the mortgage. The strategy of using the side-fund and possible structures for that is a whole other conversation. Just suffice it to say, it’s possible to create a low-risk side fund to store the money, have it grow over time and retain liquidity.

So, bottom line is, yes you can prepay a mortgage, eliminate interest in excess of your prepayment amount and earn a return of approximately whatever the % rate cost is on the loan you are prepaying — with the savings being realized on the backend of the loan.

It has been my experience that while paying interest forward this way certainly works…..You as a borrower are subject to the process your servicer uses to apply your prepaid mortgage interest payment. I have mortgages with Wells Fargo and Bank of America…..and both have screwed this up for me. As such, it is important that you stay on top of the payment and ending principle balance like a hawk….cause they will surely mess it up….even though numbers are numbers and should match up, in my case, it was almost like getting a congressional salary reduction bill through Congress to get the these servicers to agree that my numbers were correct. And even after they agreed to my numbers….they still get it wrong….it’s as if they are waiting for me to say the hell with it…..

I’m not sure about the interested saved the next month but paying off the mortgage early would save $553,012 in payments….that alone makes it worth paying extra.

I agree with Stan. There will be a savings whenever you pre pay on a simple interest loan. However, it won’t be 2800 bucks in one month by pre paying 1200 the month before. Get some sleep my friend. 😉

Sorry, interest on the principle never stops until the note has been paid in full. By making the additional principle payments during the year you will reduce the principle for 1/15 and the interest paid will be less then the table but still there will be interest paid.

Stan